Housing Starts and Building Permits:

May (Tuesday)

Housing starts fell more than 15 percent last month, well below expectations, bringing the pace of new home construction to its slowest level since 2020.

- Expected/prior housing starts: –2.0%/–8.5%

- Actual housing starts: –15.4%

- Expected/prior building permits: –0.9%/+4.5%

- Actual building permits: –0.7%

Retail Sales:

May (Wednesday)

Retail sales growth beat expectations last month. Although some of the improvement may be due to larger tax refunds this year, it remains an encouraging economic sign given the importance of consumer spending.

- Expected/prior monthly change in retail sales: +0.6%/+0.4%

- Actual monthly change in retail sales: +0.9%

Federal Open Market Committee (FOMC) Rate Decision:

June (Wednesday)

As widely expected, the Fed left interest rates unchanged after its June meeting. The post-meeting statement and Warsh’s news conference, however, were viewed as hawkish by investors.

- Expected/prior federal funds rate upper limit: 3.75%/3.75%

- Actual federal funds rate upper limit: 3.75%

Equity

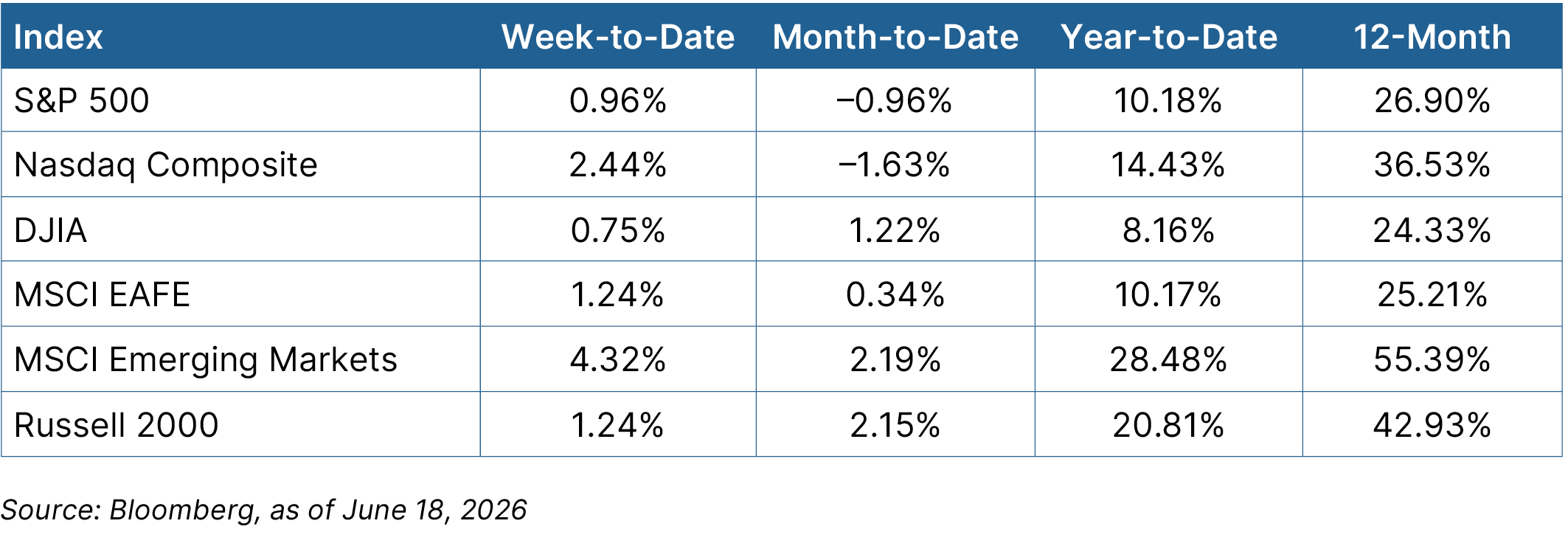

The signed MOU between the U.S. and Iran helped drive markets higher. The technology-heavy Nasdaq Composite led the way, rising 2.44 percent. From a sector perspective, technology and industrials each rose nearly 3 percent. With the Strait of Hormuz poised to reopen and oil prices declining more than 10 percent, energy fell 6.5 percent. Real estate, health care, and consumer staples each sold off roughly 3 percent. International markets continued their strong performance.

Fixed Income

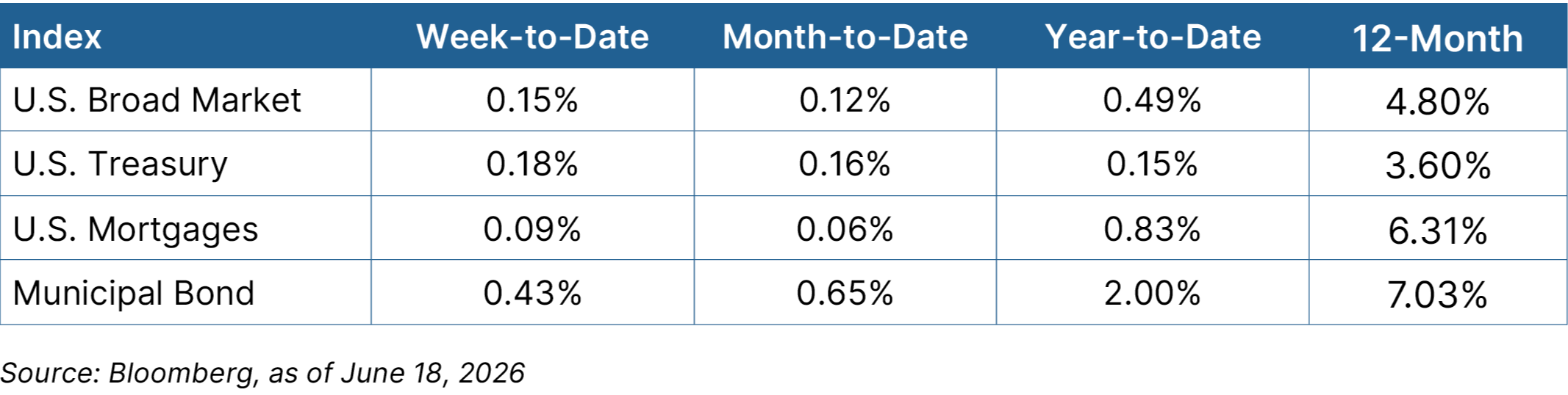

Bond markets were up marginally despite investors interpreting the Fed’s meeting as hawkish. The central bank, which remains focused on reining in inflation, left the door open for a potential rate increase this year. Short-term Treasury yields rose, and longer-term yields declined, with the 10-year closing at 4.45 percent.

Looking Ahead

The highlight this week will be the release of personal income and spending data for May.

- The week kicks off on Wednesday, when Micron reports earnings for its May quarter. Micron has been a big beneficiary of the AI buildout, and investors will be focused on the outlook because the company has been one of the biggest drivers of corporate profits this year.

- On Thursday, we’ll see the preliminary durable goods orders report for May. Orders are expected to decline sharply because of weakness in volatile transportation orders.

- Also on Thursday, the personal income and spending report for May is expected to be released. Both data points are expected to show growth, which would represent a solid rebound after a flat April.